EXECUTIVE SUMMARY

If question WHY is answered perfectly ,answer to question HOW is easy & automatic. Why a Tax Regime is to be selected is analysed along with, HOW is also answered.

Now that New Tax Regime has become Default.

(By the way, it is default, mainly because of open secret that number of frauds were committed by tax payers claiming all types of deductions & tax exemptions based on bogus & fake receipts & that is why for government benefits, these tax deductions & exemptions are totally scrapped in New Tax Regime, it is for their benefits, not for us-the Tax Payers)

It is imperative to critically analyse both tax regimes with respect to Wealth Creation & Financial Independence Goal at Retirement Age.

Main advantage of New Tax Regime is-NO COMPULSION TO INVEST IN TAX SAVING INVESTMENTS TO SAVE TAX. So surplus cash available to spend increases significantly.

But COMPULSION TO INVEST IN TAX SAVING INVESTMENTS TO SAVE TAX, if judiciously planned can definitely help for Wealth Creation & Financial Independence Goal at Retirement Age.

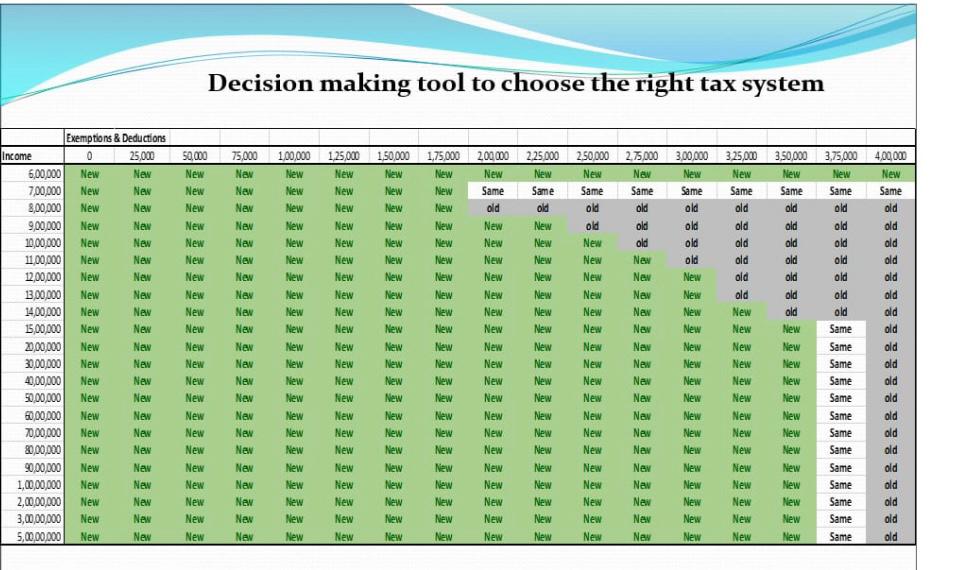

Basically up to a limit, Tax Burden in both Regimes remain same if compulsory deductions & tax exemptions are fully utilised.

Beyond limit also, Goal of Wealth Creation & Financial Independence Goal at Retirement Age, can be very well fulfilled if same Tax Saving Investment Options are judiciously utilised.

One can identify these limits by comparing New & Old Tax Regimes, available ,as Calculators, free, on internet for Oneself, as it would vary from Person to Person.

New Tax Regime has following message, in between the lines for Tax Payers.

DO UNDERSTAND IT WELL.

Government has received its Tax, now whatever you want to do with your money, it is your headache, invest wisely or unwisely as you wish or spend as you like. Government is not interested in your Wealth Creation or Financial Independence at Retirement Goal. It is your money, your future, your concerns.

But Individually One is interested ,definitely, in Wealth Creation & Financial Independence Goal at Retirement Age.

For these reasons, how Old Tax Regime can be helpful is discussed hence forth.

There is an idiom- to hit two birds with one arrow, in other words, Single Effort & Double Results, Less efforts & More gains.

There is Arth Sutra which states that Tax Saving should not be First Goal in Personal Finance, it is the Last. These two commandments are guiding principles, based on them; I will recommend Tax Saving Products that serves both the purposes- as Tax Saving & as Retirement Products.

Even when Sachin Tendulkar retires, Mahindra Singh Dhoni also retires, one should not live in fool’s paradise to be fit & be able to work till last breath.

If One is certain to die someday, One is certain to become Old few years before death.

So be it New Tax Regime or Old Tax Regime, Retirement Planning is Mandatory.

Tax Saving Purpose should be aligned with Long Term Goal of Retirement Fund Creation.

So if there are products with Long Term Lock In, it should be a welcome feature.

They are

- PPF

- ELSS

- Retirement Oriented Mutual Funds –ROMF in brief

- NPS Tier 1

- There can be one more, Insurance Companies offered Unit Linked Pension Plans– ULIPP– but they are costly & basically they mimic ROMF, which is better than ULIPP, so omitted.

I will not try to reinvent the wheel.

Basic features of all 4 schemes are well known to everyone. I will simply highlight their features that are relevant to Retirement Planning. They all offer same tax benefits, except NPS, which has special benefits under 80CCD 1 B & to avail this benefit, One has to invest in NPS Tier 1. So it becomes compulsory component of every option that I will discuss later on. It is not that one of the options is Best & One must invest in it.

Remember there is NO BEST INVESTMENT PRODUCT for us; there is ALWAYS an APPROPRIATE INVESTMENT PRODUCT for a particular purpose (Retirement Planning) for us. My guidelines are to help One select an APPROPRIATE product for Oneself, not the BEST one.

I would not rate any product, I would offer options & One will decide appropriate option for Oneself.

PPF. is oldest one, government guaranteed, totally tax free at entry, earnings & exit stage, and total lock in for first 6 years. It can be extended any number of times, in blocks of 5 years, once compulsory first 15 years of investment is completed. Low returns product, subject to revision every quarter by government. I have seen its return going down from 12% once upon a time to current return at 7.1%, but it may go down in future.

It lends stability to portfolio, being a Debt, government guaranteed product. Also helps in rebalancing portfolio in extreme times of Equity Markets. Also helps when Equity part needs to be reduced in closing years to Retirement. Also good for small ticket investors or who are unwilling to bear Equity Markets Volatility. But it does not help to create adequate enough corpus on its own, due to low returns. Also one should continue it for very long enough time so that compounding starts yielding excellent returns & that happens in later years only. Never close PPF Account, once started. Its tax free interest makes it attractive, even in later retired years, when withdrawal starts.

Money speaks only one language:

If you save me today, I will save you tomorrow!

Don’t worry about the amount of money you need to invest.

Just start investing.

Compounding works even with ₹1.

“Money makes money.

And the money that money makes,

makes more money” – Benjamin Franklin

ELSS. is 100% equity product, subject to equity markets volatility, shortest lock in period of 3 years, likely to yield much better returns than PPF in favourable equity markets, but not guaranteed, even subject to capital erosion, also ,in adverse Equity Markets Conditions. Though in long run of decades, equity usually outperforms. To build adequate enough Retirement Corpus, exposure to Equity is compulsory. It may not be appropriate with very low investible funds or very low risk tolerance.

ROMF. also offers 80C Tax Saving Benefits. They have broadly 3 variants, Equity only, Equity Aggressive Hybrid, and Conservative Debt Oriented. They have lock in for 5 years. Out of these 3 variants, I concentrate only on Equity Aggressive Hybrid. The Logics behind this selection is as follows.

Simple, for 100% equity, we have better option in ELSS & for conservative debt, PPF already fills gap. Advantage with Aggressive Equity Hybrid Variant is in form of in built portfolio rebalancing in extremes of Equity Markets, that too, in most tax efficient way, as scheme is mandated to maintain defined Equity Debt Ratio Steady. It is more suited for Moderately Aggressive Investors. Over decades, they prove more stable & do not fall behind a lot in respect to ELSS.

NPS. It is youngest one, but promising. It has special provisions of tax relief under 80CCD1B, so DO invest at least 50000 Rs. This compulsory exposure, coupled with experience over a decade will help One decide, as to, should One increase investment or not. Always go for direct option, ENPS; always invest through D Remit facility & Virtual NPS accounts to have same day NAV benefits. It has lowest Expense Ratio in Entire World. In its short life of 15 years ,so far ,for All Citizens Model, there have been many amendments but so far they have been investor friendly & will remain so over years as well, as its subscribers will be at par with EPFO subscribers, an influential vote bank. Younger ones can go for Auto Aggressive Option with up to 75% equity exposure, while elderly ones can even go for 0% Equity Exposure. It offers wide range for Assets Allocation amongst Equity, Corporate Bonds & Government Securities to suit one’s Risk Profile & Age. May be in years to come, PRAN (Permanent Retirement Account Number) may become synonymous with PAN or AADHAR number. May be, it could be PRANVAYU for Senior Citizens. Everyone needs to have it. I have written a special blog post for NPS itself, do explore it for all & more details.

Now I offer various options based on permutations & combinations of these products.

| Option | Type of Products | Suitable for | Category Label | |||

| NPS | PPF | ELSS | ROMF*With Hybrid Equity Aggressive Option | |||

| 1 | 25% | 25% | 25% | 25% | Any & Every Age | Well Diversified Moderate |

| 2 | 100% | 0% | 0% | 0% | Old | Actively Adjusted as Appropriate |

| 3 | 25% | 75% | 0% | 0% | Age 50/50+ | Conservative |

| 4 | 25% | 0% | 75% | 0% | Age 20-40 | Aggressive |

| 5 | 25% | 0% | 0% | 75% | Age 40-50 | Balanced |

| 6 | 25% | 0% | 37.50% | 37.50% | Any & Every Age | Aggressively Balanced |

*ROMF – Retirement Oriented Mutual Fund.

Notes for the above Table:

- 200,000 Rs. Total tax deductible investment amount divided into 4 parts, 80 C part 1,80 C part 2,80 C part 3 & 80 CCD 1(B), each one as 25% or 50000 Rs. One can change total figure & accordingly each part.

- These 6 options are only examples, depending upon one’s own approach, risk appetite, risk tolerance one can modify as per one’s choice, only after understanding all products well.

One who approaches life in a balanced way, should go with option 5.He would prefer enough funds also, but not at cost of high volatility, so compulsory 50000 Rs in NPS 1 & rest 150000 in ROMF is choice.

Those, who enjoy risk; believe that Ishq hai to risk hai. Should prefer option 4, full 150000 in ELSS only.

Those who have limited funds, for them it is better to play safe, stay invested in government guaranteed PPF, option 3.

Those, who earn good enough, let them take middle approach, and be equally divided between ROMF & ELSS, option 6.

Now about my choice, at my age of 62 years of life, completed.

I have faced more odds than many, am Senior Citizen also. I prefer calculated risk. So far I have been with option 1, equally divided among all 4 investment options.

My Rationale for Option 1 adopted so far is as follows.

Not very complex, NPS & ROMF placed at other ends, with automated rebalancing or profit booking or timing markets, whatever way label it, doing their job & steadying my portfolio. I did same job, myself, actively using PPF & ELSS as two different asset classes. Overall I did not miss opportunities, nor did I get kicked out of Retirement Corpus Generation Plans. As Simple As that.

Now I have switched to NPS Only for entire 2 Lakhs, with 50% Equity (Maximum permitted in NPS beyond age 50) & 50% in Corporate Bonds.

To Conclude,

I share some Pearls of Wisdom in Personal Finance.

“Lifetime investment returns are not a matter of skill.

They are a matter of behaviour.” – Carl Richards

3 Things To Remember In Your Investment Journey

Do your homework to find the facts and reasoning before investing. Don’t get carried away by public opinion or Expert opinion.

You’re becoming a matured investor if your mind can keep two opposing investment views without any hatred.

‘Planning to start investing’ and ‘Starting to invest’ are entirely different things.

Tax Saving Purpose should be aligned with Long Term Goal of Retirement Fund Creation.

So if there are products with Long Term Lock In, it should be a welcome feature.

To add in Conclusion,

I share as to how New Socio Economic Stratas have evolved over last few decades.

Old age Social classes, like, Poor, Lower Middle, Middle, Upper Middle, High Net Worth & Royal Rich now stand outdated.

Instead there are only 3 Socio Economic Stratas

I will name & characterise them.

(1)Totally Dependent.

Lowest Strata, fully dependent on Government Subsidies, not eligible for any kind of Bank Loans.

Always going to Money Sharks for Loan.

(2)Dependent

Eligible for Bank Loans & heavily EMI Burdened, Always Dependent on Salary or Earnings to pay EMIs.

Life in the absence of Salary or Earnings is a nightmare.

(3)Independent

Highly eligible for Bank Loans, but, 0 Loan amount.

No liability, No EMIs to pay.

Not worried about Salary or Earnings as Livelihood & Life Style Expenses are managed from passive income sources, like Rental Income, Dividends, Interest Incomes, Capital Gains, Safe & Sustainable Withdrawal from Accumulated & Appreciating Wealth.

Let us strive to rise to Independent Strata.

Forget Old Age Social Stratas & Get aligned with New Stratas as characterised.

New or Old Tax Regime, whatever one opts for, but Assets Building for Retirement Planning & Wealth Creation to move into Independent Strata is Mandatory.

If One is prudent enough to align Tax Saving Measures with Wealth Creation Measures, Old Tax Regime is equally beneficial.

While with New Tax Regime, with No Mandatory Tax Saving Measures, if One ignores Wealth Creation Measures, Life will definitely throw more challenges in financially tough times.

So the Younger Generation must be careful with whatever Regime One selects & deployment of available Money Resources.

As Simple As That, Sirs.

excellent narration of financial wisdom

Good work sir. Balanced and non bias, as always.